Big news recently, as Publicis acquired retail media platform Citrus.

We detailed how these platforms are typically used in a recent article. The acquisition by Publicis puts a different spin on it.

Beyond the outright purchase of the tech, Publicis has mentioned it plans to use Citrus as a compliment to its identity solution – CORE ID – which was born out of their acquisition of Epsilon. Citrus would fuel the on-site data, while Epsilon would handle off-site, with both connecting via their CORE ID product.

Regardless of how it all plays out, it’s an acquisition meant to a) capitalize on the retail media boom and b) combat the eventual decay of the third-party cookie. Publicis is looking to gain—in the near-term—via sponsored search revenue and—in the long-term—via access to deterministic, first-party data.

What We Know

Citrus Will be a Stand-Alone Product within Publicis

We’ve been told it will sit under Epsilon in the product hub. They already have safeguards in place to firewall their information, with the near-term goal being to grow the product via the roadmap.

The Acquisition Will Advance Citrus’s Product

Having a parent company with deep pockets isn’t a bad thing for a tech company looking to focus on development. Citrus should be able to catch up to the likes of Criteo in relation to functionality and clout in short order. Before this acquisition, that was not a guarantee. Citrus also now has the financial backing to legitimize their “no tech fee” stance to sponsored search. One that differed heavily from Criteo’s “duh, of course there’s a tech fee” approach.

Citrus’ Relationship with Its Clients Won’t Change (Initially)

Advertisers will still be able to buy sponsored search ads through Citrus on their preferred retailer. Publicis will not interrupt those interactions. It could go a lot of different ways in the long-term, but all near-term signs point to maintaining the status quo.

What We Don’t Know

How Data Really Plays into the Arrangement

There’s been chatter around how Publicis will use the data. In reality, though, they’re purchasing ad tech that layers onto a retailer’s site. In the case of Roundel and Citrus, the all-important first-party data is, and always has been, Roundel’s data. A retail media arm like Roundel isn’t in the data sharing business, they’re in the data selling business. Any data connections would presumably be made at the source (i.e. Epsilon partnering with Roundel).

Each Retailer’s Intentions

There had to have been at least some thought put into the duration of the agreement between Citrus and its retailers. The underlying thinking across retail media was platforms like Criteo, Citrus, Quotient and others had a limited shelf life as it relates to the larger retailers. They’re bolt-on technology that could eventually be replaced by the retailer’s in-house efforts. One has to assume Publicis was keen to this, knowing both Amazon and Walmart have built out similar, in-house sponsored search offerings. There was likely some variety of long-term language built into the contract meant to bind Target (and other retailers) to Citrus’ technology.

What’s Next?

Retail media is growing aggressively, especially within the sponsored search realm. Citrus’ retailer roadmap has added 18 retailers thus far this year alone. They’re going to be adding headcount within both sales and development, shoring up their product, and getting ready to capitalize on what is a burgeoning industry.

The only thing that can hold them back in the near-term is the philosophy of their retail partners. When you look at the search offerings of an Amazon or a Walmart, they’re designed to drive spend. They’ve created competition heavy ecosystems (i.e. paid ads in the top listings, no safeguards against conquesting, etc.) that have proven highly successful.

Target’s sponsored search efforts, on the other hand, still focus on the idea of incrementality (only organic listings can own top spots) and safety (no conquesting allowed). These focal points are music to the ears of any advertiser, but as an ad tech company tied to this approach, you have to think Citrus, Criteo, and now Publicis, are hoping for a change of heart from Target.

BigCommerce acquired Feedonomics late last month in a move that provides the ecommerce giant with a dedicated, full-scale feed management solution. It’s a play designed to cash in on ecommerce’s expanding role. With a solution like Feedonomics in-house, BigCommerce can better extend beyond direct-to-consumer, connecting its user base to the commerce functionality across the search engines, social networks, affiliates and retailers that can further grow their business and other businesses big and small.

Why is Feedonomics such a valuable tool in the BigCommerce arsenal?

Feedonomics was previously a product that could integrate with BigCommerce’s platform, but now it will be part of their in-house product suite. The acquisition combines a best-in-class feed management solution with one of the top—if not the top—commerce platforms for large enterprises. BigCommerce can power the commerce functionality onsite, while Feedonomics can ensure accuracy when selling offsite. The offsite portion is a lot larger than most realize, extending to search engines, social channels, retailers, etc.

BigCommerce has commonly built itself around integrations, but an acquisition of this nature makes a lot of sense. They know their customer base is selling both onsite and via retailers. Providing a built-in solution like Feedonomics makes it easier for their clients to sell products online, regardless of channel. The acquisition is also a move designed to help fend off Shopify (more specifically Shopify Plus) as it relates to enterprise-level business. Shopify, which is more dependent on app integrations when scale is necessary, can’t compete at present with the addition of an advanced, deeply product-focused, built-in solution like Feedonomics.

And despite both being larger offerings often focusing their efforts on larger players, BigCommerce has noted an eventual self-serve version in the works for small businesses looking to deploy Feedonomics. Thus, making the platform much more attractive to SMBs looking to manage their efforts in-house on their terms. As of now, Shopify has the upper hand in sheer customer volume, with more than a million businesses, albeit often smaller ones, using its platform. This acquisition makes BigCommerce an even more enticing option for the other end of the spectrum—the large-scale enterprise—by enabling them to grow their customer base by selling via more avenues. And as the self-serve option rolls out, it will be worth monitoring the number of smaller businesses that flock to or launch with BigCommerce and the impact it has on those businesses’ operations.

Cincinnati’s Largest Ad Agency is also the Top Agency to Work For

CINCINNATI – (August 12, 2021) – The Enquirer Media recognized Empower on its roster of Top Workplaces for 2021. Based solely on anonymous employee survey responses led by a third-party employee engagement platform (Energage), Empower is the only ad agency to make the list.

Empower CEO Jim Price Says, “This award reinforces the supportive culture we have at Empower. Future leaders should take note: when you take care of your people, they take care of your business. We’re on track to experience our best year yet and it’s because employees know they are more than a number at Empower. We nurture people’s passions and career development, allow them to dust themselves off and learn from challenging times, all in an effort to inspire each other to live an empowered life.”

About Empower Media

America’s largest woman-owned media agency

Our advantage is simple: Clients first – not shareholders.

From the day we opened our doors in 1985, Empower has always challenged the media status quo.

Empower is a highly awarded and respected media agency. We are a multi-year recipient of “Agency of the Year” from MediaPost and Campaign US with honors from Ad Age and Adweek.

Our senior and experienced integrated team of Communications Strategy, Media Innovation, Media Planning and Buying, Creative, Marketing Scientists, Influencer Marketing and Data-Analytics work in collaboration on our client’s business daily.

Empower’s client tenure rate is unmatched–3X the industry average. Our clients include Tempur Sealy, Wendy’s, Brooks Running, Fifth Third Bank, Gorilla Glue, O'Keeffe's, E.W. Scripps, Jack Link’s, VTech, Bush Brothers, Zaxby’s, GNC, Famous Footwear, Ashley, LIXIL, O-Cedar, Rust-Oleum and RoC Skincare.

Empower Media is woman-run (67% female) and woman-owned – making it the largest woman-owned media agency in America.

Our offices are in Chicago, Cincinnati, Atlanta, New York, Houston and Palm Beach.

For consumers, it’s the “most wonderful time of the year,” but for marketers, it’s crunch time. While we’re decking the halls in the physical world, the digital space is bursting at the seams with brand ads, discounts, giveaways and gift guides from brands determined to drive sales. Shoppers have endless options. Brands, on the other hand, struggle to stand out.

Our CultureTap Holiday Content Planning Guide highlights key trends, themes and strategies that can help home category brands’ digital marketing approaches shine this holiday season.

CultureTap is Empower’s trend identification platform, which helps brands participate in moments that matter. Unlike social listening tools, CultureTap isolates relevant cultural, category, brand, or competitive trends so smart marketers can act before it is too late.

Our Host

Leigh-Ann Bortz, Senior Director of Product Development

It carries a weight unlike anything in ecommerce. This past year, despite every circumstantial pitfall thrown its way, it still managed to be a roaring success for Amazon. Every year it seems to have grown in scope, importance and potential for Amazon, the key phrase there being “for Amazon.”

Success on Prime Day is almost a guarantee for Amazon. They’re going to see elevated visitor totals, elevated conversion rates, elevated revenue, etc. The same can be said for sellers on Amazon. They’ll see more interest in their products, more product detail page (PDP) views converting to sales, and more revenue than the average day.

But Amazon is the only party that will see a guaranteed increase in the all-important lever of profitability. Sellers might see heightened revenue, but they may not necessarily see profitability tied to those revenue totals improve.

In the end, Amazon is the only Prime Day participant guaranteed to receive a jolt to its bottom line. Which begs the question: Is Prime Day really all it’s cracked up to be?

What’s Working in Amazon’s Favor

Prime Day is Officially Flexible

Prime Day has historically occurred in July. In 2020, Amazon ran into issues meeting consumer demand in Q2 – throwing that timing for a loop. This, combined with a variety of other pandemic-related factors, led them to postpone Prime Day, pushing it to Q4. Despite the move, that iteration of Prime Day was Amazon’s most successful to date.

2021’s version – despite being moved once again to June – followed suit. Adobe estimated total Prime Day sales surpassing $11 billion, representing a 6.1% growth compared to 2020. Staggering numbers for an event that was born a mere six years ago.

But YoY growth aside, there’s no doubt the timing of the 2020 version of Prime Day eroded sales that were destined for holiday timeframe. The true value of Prime Day to Amazon is its position within the calendar year. It’s a made-up event positioned smack dab between the prior and upcoming holiday seasons.

The Hype Surrounding Prime Day

Creating a reason for consumers to spend mid-summer was a genius move. It gives the Amazon hype machine a chance to build up a frenzy of buying during an otherwise dormant shopping timeframe. One which the retail industry has forever been trying to figure out.

The funny thing about the past few Prime Days has been how little Amazon has needed to promote them. For example, their unwillingness to publicly confirm a date leading up to 2020’s event led to a flurry of speculation and media guesswork. It seemed there was a new “We Think Prime Day will Occur on [Insert Date Here]” storyline almost daily across an ever-rotating list of publications.

Amazon’s unwillingness to reveal details – in an era where people (and companies) are all-to-eager to share everything online – drove people wild. It was yet another genius move, letting the ambiguity drum up anticipation. Why commit to a date if everyone was constantly publishing content around how they had yet to commit to a date?

The Illusion of Prime Day

Regardless of when it occurs, Amazon has found a way to paint Prime Day as a can’t miss event for everyone. This has led sellers to view it with a siloed, self-involved lens. But what these individual sellers often don’t consider is that Prime Day isn’t solely their day. As noted, it’s an event for everyone.

Everyone is anticipating huge volume spikes and revenue gains. You and your competition come into Prime Day with the same mindset – to capitalize. But at what point does the need to capitalize outweigh the need to not get swept up in the moment?

Amazon tells sellers to expect an uptick in volume and willingness to convert from consumers. Thanks to this uptick, everyone should see revenue gains. What Sellers often see though is a different picture than the one painted by Amazon. Heavy competitive pressure (mostly via paid ads) tends to make capitalizing on Prime Day an uphill battle.

What’s Working Against Most Sellers

Reliance on Paid Ads

Prime Day is merchandised as the end-all, be-all online event. Designed to drive volume and efficiency for every seller willing to plan around it.

In the case of organic traffic, this is 100% true. Prior to Prime Day, sellers need to have their organic house in order. Product detail page (PDP) content, inventory levels, product catalog accuracy, pricing expectations and more need to fully optimized to capitalize on Prime Day. But in the last couple years, it’s become more and more apparent that relying on organic just won’t cut it.

The paid advertising model has taken Amazon by storm, and its fully designed to wreak havoc on Prime Day. For example, Amazon’s approach to paid ads not only allows conquesting; it encourages it. There is nothing keeping an advertiser from bidding heavily on terms and ASINS designed to steal share from the competition. This conquesting-first approach makes an event like Prime Day all-the-more difficult to navigate.

Bid Up or Else

Every advertiser is under the impression Prime Day is theirs for the taking. There’s volume to be had, and they need to capitalize or else. To accomplish this, they need to a) defend their turf and b) conquest the competition. How do sellers achieve both? By bidding up on their most viable terms, of course.

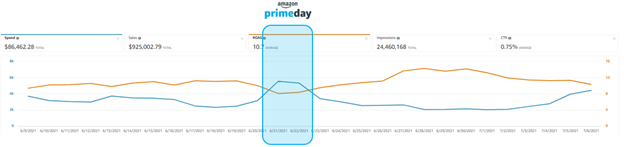

The below image shows a typical client spend and ROAS trend during Prime Day. Spend and volume increase while ROAS drops off. The reason is simple; both you and your competition are bidding more aggressively than normal, making it harder and harder to win an auction.

The expectation is that more consumers show up for Prime Day, which is true. But it’s not just you trying to capitalize on that volume. Your competition is there as well. And the rise in volume over the last few years has seemed to be offset by a rise in competition. So, while there are more conversion opportunities, there are also more sellers vying for those conversion opportunities.

Sellers expect to see huge volume gains during the two-day event and often do, thanks to spikes in consumer interest and purchase intent. But, the lulls in the days leading up to and following Prime Day can offset even the biggest of two-day gains. Prime Day’s results tend to resemble a bell curve when viewed over a longer period. The volume does not live in a vacuum, it ebbs and flows.

How to Navigate the Chaos

Approaching it with a steadier, less hype-driven mindset can help sellers in the long-run. As noted, there’s only one constant winner on Prime Day, but here are a few guideposts to ensure Amazon isn’t the only one capitalizing on the event:

Ensure Organic Presence

As discussed, getting your organic house in order is of the utmost importance. The best interaction a brand can have on Prime Day is one that doesn’t require them to pay for a click.

Deal in Deals

Take advantage of the tools Amazon provides for organic sales: Lightning Deals, Deal of the Day, Best Deal, etc. They’re well-oiled machines that require minimal investment (a nominal fee) to opt-in.

Use the Reps to Your Advantage

Within highly competitive categories, it might not hurt to go less aggressive during Prime Day and instead spread spend out over a less competitive timeframe when CPCs are more forgiving.

Be Strategic with Paid

Overstock, end-of-season, end of life, poor selling, etc., these products can all be pushed aggressively via Amazon Search and DSP before, during and after Prime Day. The products that typically sell are going to sell, but how you price and push the products that typically don’t sell can be a difference-maker.

Strive for Upsell / Basket Building

Speaking of products that typically sell, feel free to team them with products that typically don’t. Sub out or upsell whenever it makes sense via sponsored search in the moment of purchase. This will encourage basket building and higher revenue per conversion.

Be Wary of the Competition

Understand your competitors. Anticipating who will be spending alongside you is incredibly important. Some areas are worth reaching for during Prime Day, while others are not. Let the competition dive into the hype head-first.

Utilize a Profitability Cut-Off

Monitoring bidding/performance throughout the day in real-time is worth the effort. If you catch yourself pushing bids up to be competitive and drive volume, you need to know when to stop. Devise a cost/conversion-based threshold, but keep in mind real-time does not mean end result. Amazon’s latency within its sponsored search platform is well-documented and needs to be accounted for.

Prime Day is Amazon’s day. They made it. They control it. They’re the ones guaranteed to profit from it. But that doesn’t mean the rest of us can’t capitalize as well.

Sponsored Search and the Impact of Third-Party Platforms

Share

Link copied

Sponsored Search has often been considered the easiest entry point for brands within the retail media landscape.

Its effectiveness varies by network, but brands can often realize strong gains from sponsored search regardless of investment size. The value derived there can then inspire the faith necessary to test other avenues offered by retailers; avenues such as on-site and off-site digital, social via Facebook, Instagram and Pinterest, and beyond. These tactics take advantage of the true selling point retail media networks have to offer – their wealth of first-party data.

The funny thing is, despite search being the early adoption tactic for brands dipping their toes into retail media, the majority of retailers still lease their on-site search technology. In fact, Amazon Advertising, Walmart Connect and Instacart are the only retail media networks that have developed their own, in-house sponsored search platforms. Everyone else uses someone else’s technology for their on-site ad serving experience.

Third-Party Sponsored Search Platforms

When it comes to third-party sponsored search technology, there are only a few major players: Criteo, PromoteIQ, Quotient and Citrus (which was recently acquired by Publicis – more on that later). They work with a variety of retailers in various ways, but their main method is serving up their search functionality for use on retailer sites.

Historically, these interactions have been a one-to-one relationship. For example, in order to buy paid search ads on Kroger’s site, advertisers have to run through PromoteIQ. To get access to Target’s search inventory, an advertiser would need to enlist Criteo. Each retailer leasing ad serving technology would lease it from exclusively one partner.

This type of interaction can obviously lead to complications. Take Criteo, for example. Criteo – up until recently – had exclusive access to the likes of Target, Lowe’s, Best Buy, Costco, Bed Bath & Beyond and more. These are huge retailers that haven’t had either the funding, resources or bandwidth to create their own ad serving technology, so they’ve had to partner with someone else. Criteo is also very unique in that not only do advertisers pay the CPC-related fees to run search media through these retailers, but they also pay a platform fee to Criteo (upwards of 25% of media, in some cases).

Everyone Needs to Profit

This is a great example of a scenario wherein everyone needs to profit from the same interaction. Criteo is making money leasing the technology to Target, but they also know it’s not an evergreen relationship. At some point, Target is going to develop their own ad serving technology, taking everything in-house. Knowing this eventuality, Criteo has every right to try to profit while it can off its technology via its agreement with Target and the aforementioned platform fee that profits (again, upwards of 25%) from every click.

And seeing as there historically has been no other way to access Target’s on-site search inventory, advertisers had to smile and eat Criteo’s platform fee. Cost of doing business, as they say.

A Leveling of the Playing Field

Enter Citrus into the Equation. Bucking the previously stated norms, Citrus, a sponsored search offering that had recently focused heavily on grocery chains, inked a deal with Target for a split of their search inventory. This split would be between themselves and, you guessed it, Criteo, which previously had a monopoly on said inventory.

The big deal here is Citrus doesn’t charge a platform fee. Advertisers simply pay for the media. They have the same serving logic and now the same access to search inventory on Target (and Lowe’s as well). This obviously complicates every advertiser’s relationship with Criteo while also leveling the playing field a bit. And recent updates point to their no platform fee approach staying put following the Publicis acquisition.

Given the Option to Choose

Search has always been an environment with few choices. With paid search, advertisers have always known it’s either Google or Bing. And let’s be honest, more often than not, it’s just Google. With this newer iteration of paid search via retail, advertisers have been given a choice, but it’s really been a choice of one retailer or another. Whether it’s Amazon, Walmart, PromoteIQ or Criteo, they all had access to exclusive inventory. You had to live and die by their CPCs, their minimums, their rules.

But now, with the divvying up of Target’s inventory, search advertisers have a divergent path they can take. And this option is going to really test the tensile strength of a platform like Criteo. One that knows it has a shelf life and has tried to profit as much as possible during that timeframe. Advertisers can immediately begin testing the newly acquired Citrus to see if they can get the same output they received via Criteo minus the platform fee.

For a real-world example of how the platform fee can truly hurt overall performance, take a product retailing at $30, converting at a 20% clip, and seeing a $1.00 base CPC via Target sponsored search. That SKU will see a ROAS of 4.8 via Criteo, and a ROAS of 6.0 via Citrus.

A Landscape That’s Changing for the Better

The recent news related to Citrus and Target has clear-cut micro implications specific to that retailer. Advertisers looking to run search via Target now have a choice of who to run with. Criteo will likely have to bend a bit by reducing (or eliminating all together) their platform fee. If this happens, Citrus will have to prove its technology is stronger than Criteo’s, which their recent acquisition by Publicis may help answer. Having the financial backing of a bona fide holding company should supercharge their roadmap, shoring up any product development inefficiencies sooner than previously thought.

There are also macro implications for the industry at large as more and more retailers join the fray. In reference to choices, advertisers can look beyond the large retailers—the Amazons, Walmarts and Targets of the world—and maybe find a more efficient play (teamed with a growing audience) via a Family Dollar, for example.

The Publicis acquisition also throws another wrench into the situation. Now players outside retail and tech are joining the fray. The meteoric rise of retail media is enticing enough on its own to bring in a variety of suitors. The acquisition of Citrus could be seen in the same light as other holding companies who have acquired or partnered with various companies they deemed essential to agency work. These acquisitions have historically provided a variety of services around retail media – from acting as the buying arm for retailer audience-driven off-site media to actually building networks from scratch for certain retailers. These moves carve out a path (initially to revenue and, potentially, to data) that others likely weren’t considering and could possibly lead to others following suit.

It’s an interesting time to be a search advertiser. Search is traditionally the tactic that’s handcuffed to one vendor. It’s always been Google or bust for paid search. Search advertisers have never really had anyone vying for their portion of the budget. Google’s stance has been, “Go ahead, give the dollars to Bing, see where that gets you,” while Bing’s stance has been, “If it’s not going to Google, then it’s probably going to us, so just let us know”.

With sponsored search in retail media, search advertisers now have a choice as to where they allot their budgeted dollars. And soon, those retailers, and their platforms, are going to have to work a little harder to get those dollars.